Agentic AI Is a Massive Opportunity for B2B Software

Februar 16, 2026

Europa

With the Cathay Capital Private Equity Tech team, we just came back from a week in San Francisco alongside the CEOs and CPTOs of several of our portfolio companies. Together, we met a remarkably diverse set of players across the AI and software ecosystem: agentic AI start-ups, new developer tools like Replit, SaaS giants like Intuit, hyperscalers like Google Cloud and Microsoft, large-scale infrastructure companies like Crusoe, and emerging players like Dyssonance. These conversations crystallized observations we’ve been building over the past several months as we’ve worked closely with our B2B software portfolio on the Agentic AI opportunity.

The timing matters. Recent announcements from Anthropic and others have reignited market anxiety around the future of SaaS. Growth expectations are being questioned, margins are under scrutiny again, and the narrative has quickly shifted to blunt conclusions such as “SaaS is dead”.

This reaction is understandable. Something fundamental is changing. But it is also overly simplistic.

At moments like this, it is tempting to lean on buzzwords or to fall into lazy commentary. I believe the opposite is required. We need to go deeper, unpack what is really being transformed, and look carefully at where value is actually moving.

Because beyond the noise, the opportunity is very real.

Our working thesis, shaped by months of portfolio work and sharpened by our conversations in San Francisco, is this: established B2B SaaS companies that own strong Systems of Record and deep domain expertise are not the victims of the agentic shift. They are among its most natural beneficiaries, provided they choose to transform not just their product, but their organization, their pricing, and their culture.

In this article, I try to unpack what that means: what is actually being disrupted and what is not, why Systems of Record remain the foundation of any serious agentic architecture, where established players have real advantages and where they face genuine threats, what must concretely change, and what this all means for a private equity investor like us.

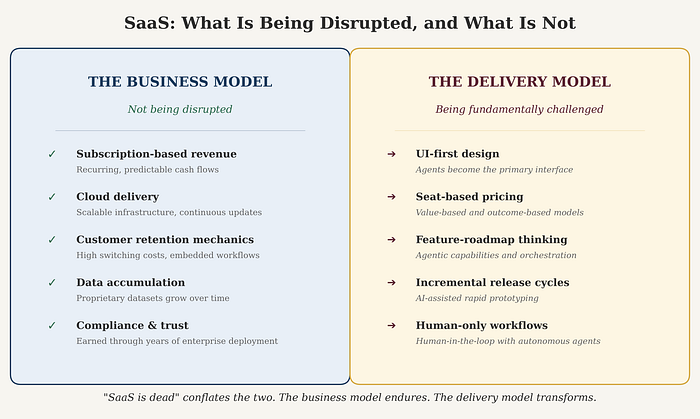

SaaS is a business model, not a product nor an interface

SaaS is a business model: subscription-based, cloud-delivered, recurring revenue. It is not a product category, nor a technical architecture. This distinction matters enormously, because what’s being disrupted is not the business model itself. What’s being disrupted is the dominant way SaaS products have been built and delivered: UI-first design, seat-based pricing, feature-roadmap thinking, and incremental release cycles.

That’s a very different statement from “SaaS is dead.”

Meanwhile, Agentic AI refers to software that can autonomously plan and execute multi-step tasks, not just answer questions (that’s a chatbot) or suggest actions (that’s a copilot), but actually do things. An agent can review a contract in Word, match invoices against purchase orders, or orchestrate an entire employee onboarding process across multiple systems. The shift from “assists” to “acts”, from Systems of Record (“SoR”) to Systems of Action (“SoA”), is what makes this transformative.

Systems of Record are not dying. Agents need them.

Here’s the thing that gets lost in the panic: agents don’t operate in a vacuum. To do anyt

hing useful, they need access to structured data, business rules, user permissions, compliance frameworks, and workflow context. All of that lives in Systems of Record: your ERP, CRM, HRIS, CLM, DAM, procurement tools, etc.

The Systems of Record are the foundation on which agents are built, not their victim.

Think of it as three layers: the System of Record at the bottom (structured data, audit trail, compliance), a Context Layer in the middle (who is the user, what are their permissions, what’s the business rule), and the Agentic Layer on top (the System of Action where agents plan, orchestrate, and execute).

The real question isn’t “will SaaS die?” It’s “who will capture the value and the user relationship?”

A fork in the road for SaaS players

Every established SaaS company now faces a choice, and inaction is itself a choice.

Path one: take the risk of becoming invisible plumbing. If a SaaS company doesn’t build its own agentic capabilities, third-party overlays will do it for them. These overlays sit between the user and the application, capture the user relationship, and gradually reduce the SaaS to “headless SaaS,” an invisible API that anyone can swap out. The consequences are predictable: pricing pressure, revenue erosion, lower Net Revenue Retention, and eventually churn. We saw this exact pattern in the early 2000s when on-premise software companies let SaaS challengers develop above them. Most of them declined, often without ever making a conscious decision to do so.

Path two: build the agentic layer yourself. At Cathay Capital, working with our portfolio companies and meeting many software entrepreneurs, we’ve been mapping what we call the “Agentic Overlay Pattern.” We see four types of agents emerging. Copilots that assist users within existing workflows, for instance an AI assistant inside a CLM tool that drafts contract clauses such as in DiliTrust suite. Wedges that own a specific job end-to-end, like an agent that handles the entire invoice-to-payment cycle in a procurement platform such as OnVentis. Sentinels that continuously monitor data and flag issues before they escalate, such as a brand compliance agent within a DAM like Wedia that detects inconsistencies across digital assets in real time and alerts the right stakeholders for brand guidelines violations or other risks. And Orchestrators that execute complex multi-step workflows across multiple tools, such as an agent that coordinates an entire employee onboarding process from HRIS to IT provisioning to training, in a digital workplace such as Powell.

The companies that choose the second path don’t just defend their position. They expand their addressable market, because agents can do work that was previously done manually or not done at all.

Established B2B SaaS companies have massive advantages

Not all SaaS companies are equally positioned. The ones most likely to benefit from the agentic shift are horizontal B2B suites that control data and workflows across multiple functions, deep enterprise point solutions that are embedded in their customers’ critical operations, and vertical SaaS platforms that combine domain expertise with industry-specific data. Thin tools with limited proprietary data will face the hardest headwinds.

These established players have five assets that neither internal development teams of their customers nor emerging agentic startups can easily replicate:

Proprietary data. Years, sometimes decades, of structured customer data, usage patterns, and domain-specific datasets. Think of a procurement suite like OnVentis that has accumulated years of supplier performance scores, pricing benchmarks, and purchasing patterns across hundreds of enterprise customers. That dataset is what allows an agent to recommend the right supplier, flag an anomaly in a quote, or predict a delivery risk. A new entrant can build a better interface, but it starts from zero on the data that makes the agent actually useful.

Deep context. Knowing who the users are, what permissions they have, how they work, what decisions they make and how they make them. This is what makes an agent reliable rather than generic. Consider a digital workplace platform like Powell that manages team governance and data access controls at scale across Microsoft 365 environments: it already knows which employee can see what, across which business unit, under which compliance rules. That context is precisely what agents need to operate safely in an enterprise. Without it, you cannot deploy agents at scale. With it, the platform becomes an essential building block of any serious agentic architecture.

Domain expertise. Deep vertical knowledge in legal, procurement, HR, finance, or industrial operations, that generic LLMs simply cannot match. An agent that drafts contract amendments needs to understand jurisdiction-specific rules. An agent that optimizes a supply chain needs to know the specific logic of lead times, supplier tiers, and substitution constraints. This kind of knowledge is accumulated through years of customer feedback and real-world edge cases. It is what makes the difference between a demo that impresses and a production agent that enterprises will actually trust.

Installed distribution. An existing customer base, commercial relationships, enterprise trust, and go-to-market infrastructure. As one Google Cloud AI leader told us bluntly: “Distribution beats features.” A SaaS suite with thousands of enterprise customers can ship an agentic feature to its entire base overnight. A startup has to sell it one customer at a time.

Proven trust and regulatory compliance. This is the advantage that doesn’t get discussed enough. Enterprise customers in finance, healthcare, legal, or government don’t just buy software. They buy the vendor’s demonstrated ability to meet audit requirements, data residency constraints, traceability, SOC 2 certifications, and industry-specific regulations. When a bank or a pharmaceutical company deploys an agent that touches sensitive data, it needs to know the vendor has been through the compliance gauntlet before. That trust is earned over years and cannot be fast-tracked.

But it’s a race, and both threats are real

Established B2B SaaS companies do face two forms of competition, and both are real.

The first is internal development. CIOs are more open than ever to experimenting with building their own agentic tools, driven by the genuine excitement around AI and the falling cost of software development. Shadow IT is flourishing. But this openness is likely temporary. As these internal projects move from prototypes to production, companies will run into the same problems they always have with in-house software: who is liable when the agent makes a mistake? Who maintains it when the underlying LLM changes? Who ensures it remains compliant as regulations evolve? The structural advantages of specialized SaaS vendors on reliability, maintenance, and accountability don’t disappear because development got cheaper.

The second is emerging agentic-native players. Some will achieve rapid initial traction by identifying a specific use case where they deliver an experience ten times better than what the incumbent suite offers. That’s real, and incumbents should not underestimate it. But to become sustainable businesses, these startups will need to expand quickly to master the broader context: accumulating the proprietary data and workflow knowledge needed to deliver deterministic, reliable outputs rather than probabilistic ones. In the B2B world, and especially in regulated industries, “it works most of the time” is not good enough. In most enterprise contexts, these startups will need to broaden their scope significantly, and will face the very data acquisition and compliance challenges that took incumbents years to solve.

There is also an economic dimension that remains highly uncertain. The cost of AI inference, and more broadly the sustainability of the massive capital being deployed into AI infrastructure, will have significant consequences on business models across the ecosystem. Agentic-native startups, whose economics depend entirely on inference at scale, are structurally more exposed to this uncertainty than established SaaS companies whose revenue base rests on proven subscription models. The margin profile of players like Lovable, whose cost of goods sold is dominated by inference costs that remain volatile, illustrates the challenge: their unit economics are far from stabilized. For an established SaaS company adding an agentic layer on top of a proven subscription business, the risk profile is fundamentally different.

In essence, what we’re witnessing is a race from opposite starting points. Established SaaS companies own the context and the data, the records, but need to build the agentic layer. Native agentic players start from the action, the user experience, but need to acquire the context and the data. Both are racing toward the middle.

But this divide is only temporary. The endgame is clear: an agentic layer that feeds on context and Systems of Record, its own or those of third parties. For established SaaS companies developing agentic capabilities, one of the most compelling opportunities lies precisely here: building agents that interact not only with their own System of Record, but across multiple enterprise systems, becoming orchestration points across their customers’ software stack. The outcome of that convergence will determine who captures the next wave of software value creation.

We have already witnessed two strategies emerging to capture this cross-system orchestration opportunity.

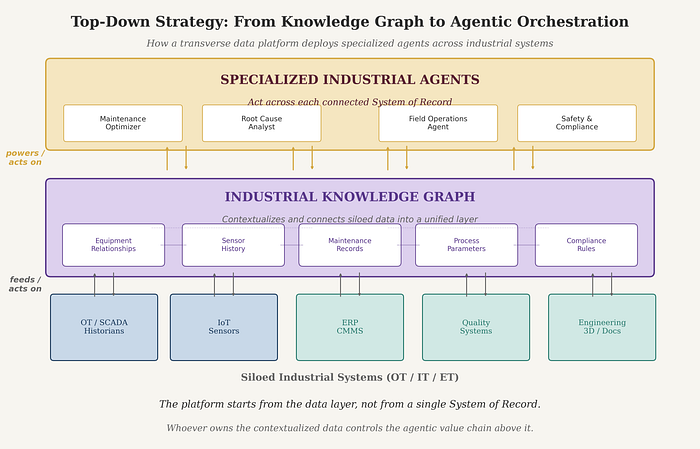

The first, which we already see at work in industrial verticals, is top-down. A platform builds a knowledge graph that contextualizes data from multiple siloed sources, operational systems, enterprise software, engineering tools, IoT sensors, into a unified layer. From this transverse data foundation, it can deploy specialized agents that act across each connected system of record: a maintenance optimizer that reads sensor data and triggers work orders in the CMMS, a root cause analyst that correlates events across the plant floor and the ERP, a field operations agent that coordinates interventions across sites. The platform doesn’t start from a single System of Record; it starts from the data layer itself, and expands into each vertical from there. Whoever owns the contextualized data controls the agentic value chain above it.

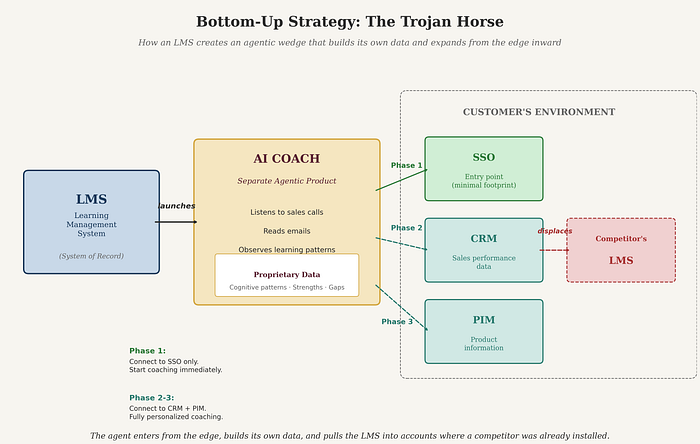

The real expansion comes when the agent connects to the customer’s CRM to correlate training with actual sales performance, and to the product information system to keep commercial teams up to date on the latest offerings in real time. At that point, the coaching becomes fully tailored and unmatched. And the LMS company that created the agent has entered accounts where a competitor’s LMS was already installed, not by displacing it head-on, but by building value from the edge inward. I wouldn’t be surprised if this is exactly the playbook behind excellence-ai.com, a Y Combinator startup that recently showed up as an AI coaching tool in my children’s school in Paris.

Both paths lead to the same destination: becoming the orchestration point across the customer’s enterprise. But the starting assets, the pace of expansion, and the competitive dynamics are very different.

The one dimension where emerging challengers genuinely have an advantage is speed of iteration: they’re built natively for the agentic world, without organizational inertia. That is precisely the dimension that incumbent SaaS companies must address. This means approaching the agentic product with a genuine startup mindset: starting from the end user, designing pricing and go-to-market unconstrained by the existing enterprise sales motion. To push the logic to its conclusion, one could imagine an established enterprise SaaS launching a product-led, even freemium, agentic wedge, lightweight enough to be adopted without a procurement cycle, valuable enough to gradually pull the customer toward the full platform. This may sound counterintuitive for companies built on enterprise contracts. But if the agent is the new entry point, then the rules of distribution may need to be rethought from scratch.

As the CEO of an enterprise SaaS company recently told me: “I’m always looking for my next freemium product as an acquisition vector.” I found that a compelling way to think about it, and perhaps worth a dedicated discussion.

What must change: it’s not just about the product

This is where the conversation gets concrete. We spent a lot of time in San Francisco digging into what exactly needs to change, and the answer spans four areas.

The interface. The SaaS web app is no longer the primary interface. Users increasingly interact with their tools through agentic interfaces like Microsoft Copilot, ChatGPT, or simply through Slack and email. Your product becomes a capability that agents invoke, whether or not it has a screen. As one AI leader we met put it: “Don’t start with UI. Agents are your new customers.” The SaaS companies that don’t integrate into these daily agentic interfaces risk losing the user relationship entirely.

That said, the traditional interface retains a value that is easy to underestimate. The UI is what creates user habits, enforces discipline in data entry and data hygiene, and provides the structured visual context needed to interpret information. Without it, the quality of the underlying data degrades, and with it, the reliability of the agents that depend on it. The shift is not from UI to no UI, but from UI as the sole interface to UI as one of several, each serving a distinct purpose.

Pricing. The shift from seat-based to outcome-based or usage-based pricing is real but won’t happen overnight. Enterprises need budget predictability. What we’ll see is hybrid models: some subscription, some usage, some outcome packaging. More fundamentally, when an agent replaces tasks that were previously handled by people, the pricing logic can shift from charging per task accomplished to charging for the value delivered. If an agent saves a company 20 hours of legal review per week, the vendor can price against that value, not against the number of API calls. This shift isn’t just defensive. It’s how SaaS companies offset the potential reduction in seat count driven by the very productivity gains that agents deliver to their customers, while expanding the total value they capture. The companies that figure this out first will have a meaningful growth advantage.

Architecture. Building for agents means building personalized context layers, accumulating proprietary data, maintaining independence from any single LLM provider (critical for cost control), and exposing capabilities through standards like MCP so that other agents can interact with your product. Your next users are machines, not just humans.

Human-in-the-loop. This is a dimension that often gets overlooked in the excitement around autonomous agents. In practice, enterprise customers will not trust fully autonomous agents from day one. Successful deployment requires human oversight at critical decision points, the ability for users to review, approve, or correct agent actions before they become final. Companies that are already the daily workflow tool for their users have a massive advantage here. A legal suite like DiliTrust that already manages contract workflows, or a DAM like Wedia that already governs content approval chains, can naturally embed agent actions into existing human review loops. That’s what makes adoption possible and what gets customers to the acceptance levels required for production deployment.

Culture, organization, and tooling. This is probably the most important transformation, and the most underestimated. It starts with how roles evolve. Product managers are already using agents to write PRDs, simulate user behavior, and conduct market research. New roles are emerging, like Forward Deployed Engineers (FDEs) who blend engineering, product, and customer context. The traditional development model, including agile, is evolving toward shorter cycles, more rapid iteration, and significantly more AI-assisted prototyping. The goal is not to abandon structured development, but to compress the time between idea and working product.

One of the most debated topics in San Francisco was vibe coding. The concept is clear: using AI tools like Cursor or Replit to prototype and build at radically higher speed. As the founder of a start-up we met through a YC seed investor told us: “We had 15 developers two years ago. We have 3 today, with AI.” But the reality is more nuanced than the hype, or at least needs to be adapted to each company context.

Vibe coding a product for customers where the priority is to ship fast and iterate, for instance the reinforcement learning tools built by the founder I am quoting, is one thing. Building an agentic product natively for enterprise clients is another, and we’ve identified a few early initiatives, including a SaaS company we’ve been discussing with over the last month that is launching its own adjacent agentic product built this way. Vibe coding within an existing product, however, does not seem realistic yet: it would require the LLM to hold the entire context of the codebase, the full documentation, and the accumulated business logic, and that is simply not possible today. We met people who think we are not so far, and this is precisely the kind of challenge that newcomers like Dyssonance are trying to address.

There is also a human dimension that deserves attention. Several of the leaders we met in San Francisco, who had deployed agents at scale to augment their teams, shared a consistent observation: while productivity increases, so does the intellectual intensity required from each individual. Working with agents is not passive delegation, it demands constant judgment, context-switching, and quality control. Early research confirms this, including a recent study published in the Harvard Business Review, which finds that AI tools tend to intensify work rather than simplify it: employees take on broader tasks, blur the boundaries between work and rest, and manage more parallel threads, often without being asked to. The implication is significant: the way work is organized, and in particular how many hours of high-intensity cognitive work a person can sustain in a day, needs to be rethought.

There is a second-order effect as well: when each individual iterates faster with their agents, the speed of iteration between humans must accelerate to match. This creates pressure to reduce team sizes, because coordination overhead between people becomes the bottleneck. Smaller teams, where each member is deeply augmented by agents, can move faster than large teams where human-to-human synchronization slows everything down. And physical proximity matters more, not less: when the cognitive intensity is high and the pace is fast, being in the same room makes collaboration significantly more effective than distributed work.

All of this makes deliberate organizational norms around AI use not a nice-to-have but a necessity, particularly for companies pushing their teams to adopt these tools at speed.

None of these transformations happen without the CEO leading by example. As a senior executive at a major SaaS company told us: “AI is a leadership transformation problem first, and a tech problem second.” You cannot decree a new culture that changes practices. Culture stems from practice, and the CEO who doesn’t personally use AI tools every day cannot credibly drive transformation across the organization.

Where the growth is going

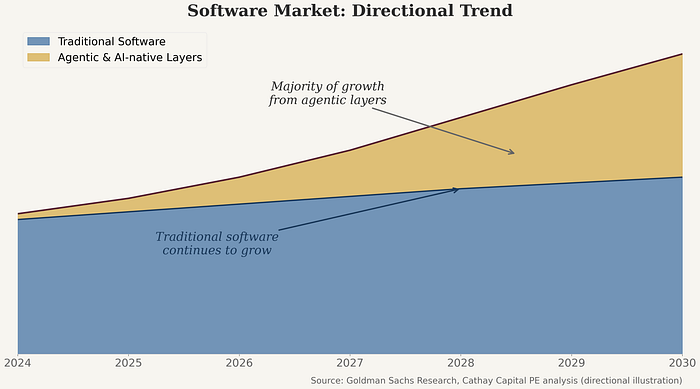

Let’s be clear about what’s actually happening. Software market growth has slowed over the past two to three years. That’s partly driven by the broader macroeconomic environment, higher interest rates, tighter IT budgets, longer sales cycles. But it’s also driven by something more structural: enterprise customers are shifting their spending and investment priorities from traditional software toward AI. The total software market is still growing, but the incremental growth is increasingly being captured by agentic capabilities, less by adding more seats to existing products.

That said, we should be careful not to overstate the saturation narrative. Many segments of the enterprise and midmarket software landscape remain significantly underpenetrated. Plenty of critical business processes still run on spreadsheets, emails, or legacy tools. And to build agentic layers, you first need the Systems of Record underneath them. There is still substantial room for growth in the foundational software itself.

What we’re already seeing is encouraging. Some SaaS companies have understood the shift and are creating significant agentic revenue streams. Salesforce reports $540 million in ARR from AgentForce. Intercom has crossed $200+ million in ARR largely driven by its AI-first product pivot. These are not experiments. These are real revenue lines that demonstrate the market is ready to pay for agentic value. Across our own portfolio at Cathay Capital, most of our B2B software companies have now developed agentic solutions that are beginning to drive upsell with existing customers.

On the demand side, we see some interesting signals. Goldman Sachs recently announced a partnership with Anthropic to deploy AI agents for accounting and client onboarding, with their CIO describing the agents as “digital co-workers for process-intensive professions.” When a tightly regulated institution like Goldman invests in embedding agentic AI into its core operations, it validates enterprise appetite beyond chatbots and copilots. But even Goldman will not co-develop custom agents for every function. For processes outside of core operations, such as HR, procurement, document management, or digital workplace, even the largest enterprises are likely to turn to specialized software vendors. And below a certain company size, the question doesn’t arise at all: teams simply don’t have the bandwidth or the expertise to build and maintain agentic capabilities internally, even for mission-critical functions. This is precisely why established B2B SaaS players sit at the center of the opportunity.

The direction is clear, even if the precise numbers are debatable. Goldman Sachs estimates the total software market could reach $780 billion by 2030, with a majority of incremental growth driven by agentic and AI-native layers. Even if these projections prove optimistic, the structural trend is unmistakable: traditional software continues to grow, but the new value creation sits on top of it. The question for every SaaS company is whether they capture that growth themselves or watch someone else do it.

We’ve seen this movie before. When the world shifted from on-premise software to SaaS over the 2010s, some companies transformed and created enormous value. Adobe moved from Creative Suite to Creative Cloud. Microsoft reinvented itself around O365 and Azure. Both saw their market caps multiply many times over during their transformation decade. Others waited, tried to protect legacy revenue, and declined, or, at best, settled into flat-revenue, high-profitability cash cows with diminishing strategic relevance.

The parallel to today is striking. But the urgency is greater: the cost of building agentic capabilities is falling fast, the barriers to entry for new challengers are lower than they were for SaaS challengers in the 2010s, and the window for incumbents to act is shorter.

Having personally watched several waves of innovation come out of the Valley since the late 1990s, one pattern holds: the Valley is often wrong on timing, but not often wrong on direction.

What this means for how we invest

I joined Cathay Capital a few years ago after a career as an entrepreneur in connected devices and smart home technology. Coming into B2B software investing with fresh eyes, and now having spent lots of hours with management teams, entrepreneurs, and industry leaders, I find myself increasingly convinced that the agentic shift reinforces our investment thesis, not undermines it. But I share these observations with humility: this market evolves every day, and certainty is the last thing anyone should claim right now.

We heard it multiple times in the Valley: there is very probably a hype phenomenon and a bubble forming, and people there are aware of it. But they are also deeply convinced that the wave is gigantic. And so they do what the Valley has always done best: build the future without worrying too much about cycles, with the conviction that innovation will address the problems it creates along the way. Nobody knows when or how the bubble will adjust. But the underlying transformation wave is massive, arguably more powerful than previous ones. For a private equity investor, that is what matters: focusing on the substance of the shift, investing through the cycle, and transforming the companies we back to capture it.

We also heard a more radical claim in San Francisco: that within a few years, artificial general intelligence would render most digital innovation irrelevant, that the AI labs would capture everything. I don’t believe it. This reminds me of the dot-com era, and more personally of my own experience as an entrepreneur in smart home technology between 2009 and 2016. In both cases, we collectively underestimated the heterogeneity of the digital and physical ecosystems through which innovation must actually pass: protocols, integrations, user behaviors, local culture and regulations, industry-specific constraints. That complexity is what has always justified, and will continue to justify, verticalized players who deeply understand their customers’ needs and deliver concrete value in specific domains.

As investors who also back companies in the traditional economy, we see firsthand the gap between tech marketing promises and ground-level reality. Deploying agentic AI at scale today still faces significant barriers. Technical ones: context window limitations and inference cost management at enterprise scale. Technico-human ones: implementing human-in-the-loop is far harder in practice than it appears in demos, because the degree, frequency, and nature of human intervention vary enormously across processes and organizations. And organizational ones: the digitalization initiated in the 2000s is far from complete, data in many enterprises remains poorly structured and partially digitalized, and change management in organizations where employees will be profoundly disrupted is not something that can be wished away. Yet clean, structured data is precisely the prerequisite for agents that can be specific, deterministic, and therefore autonomous.

This reality, paradoxically, reinforces the opportunity for established SaaS companies that already have their customers’ trust and a deep understanding of their operational context. It also opens two adjacent investment fields that go beyond the scope of this paper: tech-enabled services that will help enterprises transform their organizations and tooling for the agentic era, and non-natively-tech service businesses, particularly in services industries, that have a window of a few years to create competitive advantage through early adoption. Cathay Capital’s platform is well positioned to accompany both, but that deserves its own discussion.

What I can say is that B2B SaaS companies that combine strong Systems of Record, deep domain expertise, and the courage to transform their product, their organization, and their culture will create enormous value. As growth equity and growth buyout investors, today we accompany B2B SaaS companies born before the agentic era through this transformation. Gradually, we will also accompany B2B software companies born natively in the agentic world. But the characteristics of a sustainable software business remain the same: deep domain expertise, strong customer relationships, recurring economics, operational discipline. We saw it during the shift from on-premise to SaaS, and we expect to see it again.

That’s an attractive investment thesis, and it’s one we actively pursue at Cathay Capital. But it also means we need to evolve how we operate alongside our portfolio companies: bringing in the right technical expertise, challenging product roadmaps, helping CEOs and their teams navigate the organizational transformation described above.

The valuation framework matters too. The era when B2B software was perceived as a perpetual growth annuity, justifying ever-expanding revenue multiples, is behind us. The 2021–22 valuation excesses made that clear. In a world where growth is no longer taken for granted, the market is gradually shifting toward EBITDA-based valuations, which is exactly how we’ve been reasoning our investment theses at Cathay for years.

The nature of software investing is changing. When the entire sector was rising, picking the right sector was enough. Today, value creation depends on the ability to identify the right companies, understand their transformation potential, and work alongside management to make it happen. Sector exposure no longer drives returns. What matters is the depth of conviction and the willingness to get involved.

Europe is a particularly interesting playing field. The regulatory environment is more demanding, and customers tend to be more conservative in their adoption patterns. That is precisely what creates the opportunity: European B2B SaaS companies that embrace the agentic transformation with the sense of urgency we see in the Valley, or in China for that matter, which we know well at Cathay, will gain a significant first-mover advantage in a market where most of their competitors will move more slowly. And because they will have built their agentic capabilities within a demanding regulatory and compliance environment, they will be battle-tested in a way that matters globally.

Cathay Capital’s platform is well suited for this. We invest in technology across three continents, from venture to buyout, and we maintain close relationships with an ecosystem of large corporates who are, in many cases, the very customers of our B2B software portfolio companies. That proximity between our investment activity and the end markets our companies serve gives us a differentiated perspective on where the agentic opportunity is real and where it is hype.

The bottom line

“SaaS is dead” is a lazy soundbite. What’s actually happening is far more nuanced and far more exciting. Systems of Record aren’t going anywhere, but the value is shifting to whoever builds the agentic layer on top. Established B2B SaaS companies have unique advantages to lead the race, provided they choose the right battlefields, transform not just their products but their organizations, their culture, and their leadership.

For those willing to do the work, both the software companies themselves and the investors who back them, this is one of the best opportunities since the cloud transition itself.

The opportunity is real. And the clock is ticking.

Selected references:

Is SaaS Dead? Rethinking the Future of Software in the Age of AI — IDC

Some Experts Argue Software Stock Sell-Off Was Too Harsh Despite AI Fears — Investopedia

Salesforce Raises Revenue Forecast as Agentforce Sales Top $500 Million — Wall Street Journal

Intercom’s Playbook for Becoming an AI-Native Business — Bessemer Venture Partners

AI Agents to Boost Productivity and Size of Software Market — Goldman Sachs

Goldman Sachs Taps Anthropic’s Claude to Automate Accounting, Compliance Roles — CNBC

AI Doesn’t Reduce Work, It Intensifies It — Harvard Business Review